NEW DELHI (CoinChapter.com) — Regular market players may have come across Grayscale Bitcoin Trust (GBTC). The world’s largest crypto fund became popular nearly a decade ago after offering an alternative solution for investors who didn’t, or couldn’t, invest directly in Bitcoin (BTC)

With the advent of cryptocurrencies to mainstream markets, GBTC soon became a beneficiary of massive investments. At one point, the fund managed $60 Billion in its kitty, which was larger than the market cap of more than half the firms listed on the NASDAQ 500.

However, the narrative took an unfortunate turn.

The emergence of Bitcoin ETFs and the top coin’s declining value lowered GBTC’s viability as an investment. Recently, unconfirmed rumors began surfacing that GBTC faced dissolution amid market worries. However, before delving into such rumors, let’s understand how GBTC functions.

Rewinding the clock

The Grayscale Investment Trust was initially launched as The Bitcoin Investment Trust in 2013 by the Digital Currency Group.

The trust allowed investments into other connected trusts which held large amounts of Bitcoin. The trust began publicly trading on secondary stock exchanges in 2015. By 2020, it became the first digital currency investment vehicle to attain the status of a reporting company by the SEC.

GBTC’s working principle is simple. First, the trust usually accumulates U.S. dollars from institutional investors and uses that to buy BTC directly. In turn, these BTC are stored in the Grayscale fund, which essentially makes the Grayscale Institution the actual owner of BTC.

In turn, investors can buy shares of GBTC and indirectly deal in BTC without owning the coins.

When Bitcoin’s bull run gained steam during 2011 and attracted new capital, it didn’t take long for GBTC to start reaping gains. By November 2021, the firm managed over a mammoth $60 billion in assets, attracting notable investors such as Cathie Wood’s Ark Invest.

An Explanation of the GBTC Model

But what made the GBTC model attractive was not only because of the BTC exposure it offered but also the arbitrage opportunities that came with it. So, to begin, let us explain how GBTC derives its value.

Like any trust that trades on a public stock exchange, an underlying asset calculates its actual value. This value is called the Net Asset Value, or NAV. So naturally, the NAV of a firm is dictated by the underlying asset’s value, in this case, Bitcoin.

Simply put, if the value of Bitcoin rises, so does the GBTC’s NAV.

However, there are instances when investing in GBTC can turn more fruitful than investing directly in Bitcoin. This set of tweets can help explain further.

Social media user @lookonchain further explains that since many financial institutions are affected by regulation and cannot directly trade BTC, they can only invest in Bitcoin by buying and selling GBTC. Hence, the demand for GBTC shares in the market is very great.

In this example, GBTC is at a premium, and investors can buy BTC and sell GBTC to pocket a gain known as arbitrage.

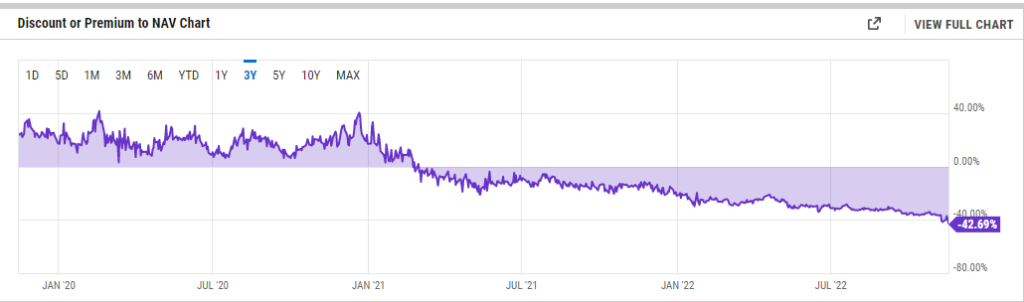

A chart highlighted below show that up until March 2021, GBTC traded at a premium to its NAV and offered multiple arbitrage opportunities. However, since then, the shares have traded constantly at a discount to their NAV.

So what changed in March 2021? Bitcoin’s bull run was very active, and based on the points above, demand for GBTC shares should have continued soaring. Unfortunately, it didn’t, because of the introduction of Bitcoin Exchange Traded Funds or ETFs.

These are pools of bitcoin-related assets offered on traditional exchanges by brokerages. Much like GBTC’s model, these ETFs offered investments into Bitcoin without directly owning them and became instant competitors.

Fast forward a year, Bitcoin’s bear market run became an increasing pain for such crypto ventures, and GBTC’s NAV continued to free-fall. As of Nov 18, 2022, its AUM had slipped to $10.8 Billion, a stark difference from the $60 Billion it managed a year ago.

Recently, Bloomberg reported that GBTC’s NAV had slipped to a record low of 42% following the FTX fiasco. In addition, rumors came to light that the troubled Alameda Research, tied to FTX, held significant amounts of GBTC.

Fears of global recession, Russia’s war on Ukraine, and rising inflation did not help.

Separately, Genesis Global Capital, a sister company of Grayscale, is also facing financial issues. The firm temporarily suspended redemptions on the platform on Nov 17. Amanda Cowie, vice president of communication, added:

“This decision was made in response to the extreme market dislocation and loss of industry confidence caused by the FTX implosion.”

In the wake of recent events, our investors should know that the safety and security of the holdings underlying Grayscale digital asset products are unaffected.

— Grayscale (@Grayscale) November 16, 2022

The decision prompted a response by the parent Grayscale firm, which assured investors that other products remained unaffected by the news.

Can it survive the market turmoil?

So what does the future hold for the Grayscale Bitcoin Trust? Will the Grayscale institution dissolve the GBTC to save its ailing Genesis unit?

@lookonchain explained that while it is possible, the same is highly unlikely.

The user explained that GBTC is a low-risk, high-yield project for Grayscale. Even when charging an annual management fee of 2%, GBTC’s annual income amounts to $210 million annually. Therefore, it’s unlikely that Grayscale would sacrifice its cash cow, at least until the market recovers.

The post Everything You Need to Know About Grayscale Bitcoin Trust and Its Dissolution FUD appeared first on CoinChapter.